After contingency amount, one has to look upon the life insurance, the most important thing towards better financial planning. now you start thinking that there are so many insurance products available in the market. Which Life Insurance Policy to Buy? Do you know the difference between term insurance and endowment insurance? This article is here to answer your long pending question. You should have life insurance coverage of at least 10 times of your annual income as per Investment guideline.

Life Insurance is required to take care of nearest and dearest ones in the event of the sudden or unfortunate demise of Policyholder. Nothing can fill up the gap of a human, but at least financials should not be the burden for them on that state of mind.

If you are the only earner in your family or the family members are solely depends on you, please take a life insurance as early as possible.

Mainly three types of life insurance products are available in the market:

-

Endowment Policies

Endowment Policies are fixed maturity insurance policies. Typically these policies have very low sum assured as these policies give some return on investment. The basic purpose of life insurance is to support the dependents of the family in case of sad demise of the sole earner of the family member.

Also Read: Know the Difference between Term and Whole Life Insurance Policies

As these policies are taking care of the return also, the premium is high and insurance coverage is less. For a Jeevan Anand Policy of sum assured Rs 5 lakhs the premium is Rs 24020, bought in 2011.

-

Unit Linked Insurance Policies

ULIPs (Unit Linked Insurance Policies) are a mixed instrument where you can get insurance coverage as well as return on investment. The basic difference between Endowment and ULIP is the return for the endowment policies are fixed and for ULIP, it is linked with the stock market. That’s why investment is risky also. For ULIPs, your investment will have the lock-in period of 5 years.

-

Term Insurance Policies

Term insurance policies are designed for the purpose of insurance only. Moreover, these policies can be bought through online also. For an insurance coverage of Rs one crore the premium is as low as Rs 7000 (approx.). If you have any extra burden such as home loan, it is always advisable to go for higher coverage of insurance.

You can also check the above figures at www.licindia.in according to your need.

There are number of insurance companies present in India other than LIC which can offer you low premium for term insurance.

Also Read: 7 Reasons Why is Term Insurance Required for You

Example: Difference between Term Insurance and Endowment Insurance

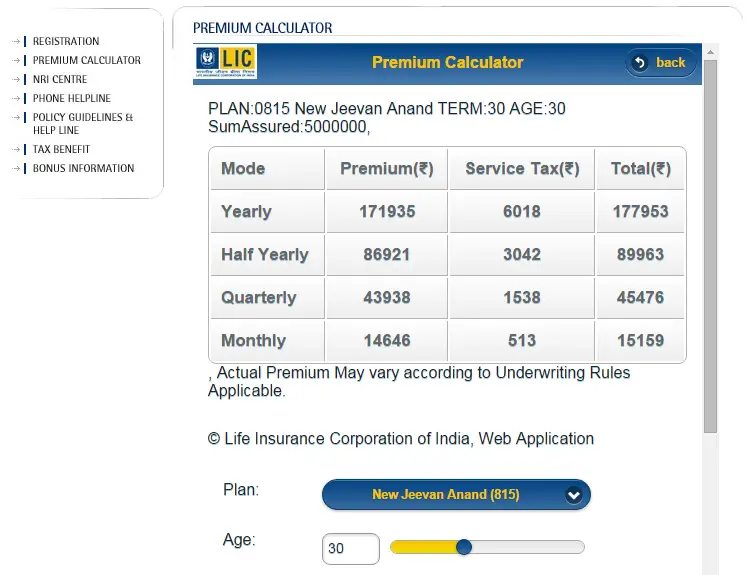

The premium for a 50 lacs New Jeevan Anand Policy the premium excluding service tax is Rs 171935 for a 30 year male for a period of 30 years. The compounding bonus is declared every year and is added to sum assured. The bonus is non-guaranteed and depends upon the profitability of insurance company. Considering all these, this policy can normally give 6-8% return on investment. The maturity amount is approximately Rs 19,477,348.

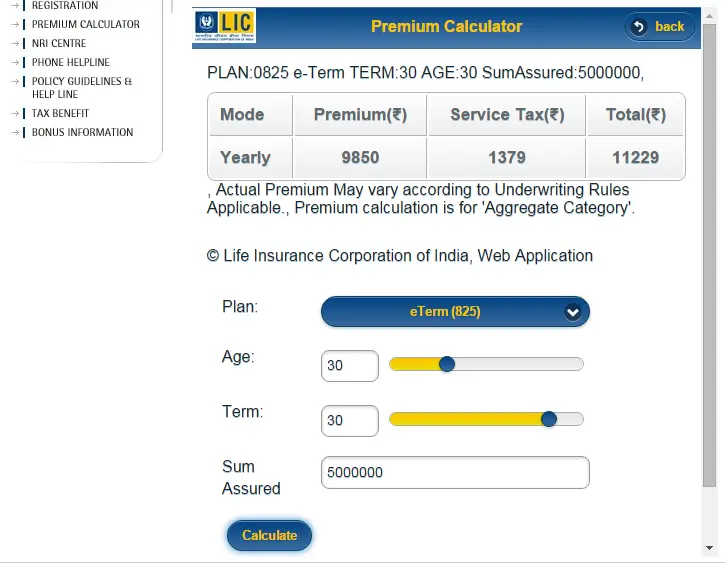

At the same time for a term insurance of Rs 50 lakhs, the approximate premium is Rs 9850 excluding service tax. The balance amount i.e. 171935-9850=162085, if you don’t invest in the endowment policy. If you invest this money in a diversified equity mutual fund for a period of 30 years, you will get Rs 30,216,784.

Those who don’t know what is mutual fund, how we can choose the fund or how we can start the mutual fund SIP, read following articles.

Hope you all have now fair understanding of the difference between term insurance and endowment insurance. Hence, my suggestion is to go for term insurance policies instead of traditional or endowment insurance policy which can cover your insurance needs as well as you can maximize your wealth by investing some money in some other instrument.

Share it with others.

{kind=link}