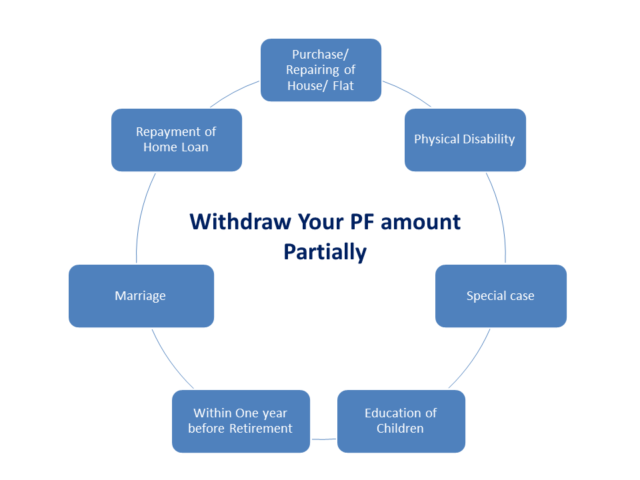

Provident Fund (PF) is the most powerful source of retirement corpus of salaried individuals. We all know that we get PF only after our retirement. Suppose, you have requirement of fund for repairing of home, the marriage of your sister or you want to prepay your home loan. Don’t worry. EPF can give you some relief in your money crunch situation on account of those reasons.

You can get a non-refundable advance from your accumulated EPF corpus. There are total nine cases in which you can withdraw PF amount partially before retirement. If you have NPS account, you can also withdraw partially from NPS account.

1. Purchase of House/flat, construction of House including the acquisition of site:

Are you planning to buy a house or a flat or do you want to buy a land for construction of your home? If you are short of money, you can withdraw some PF amount to fulfill your wish.

The following cases are applicable for PF withdrawal:

- Purchase of house/flat/construction of house including acquisition of site from Agency

- Purchase of site for construction of dwelling house/purchase of house/flat from Individual

- Buying of dwelling house/flat on ownership from promoter

- Construction of house on a site owned by member/spouse/jointly by member & spouse

For the above point a, the payment will be directly done to concerned agency. For other cases, the amount will be paid directly to the member.

You have to complete at least five years as EPFO member to be eligible for this withdrawal and you are allowed to withdraw one time only. For the construction of the house, it may be with multiple installments as required.

The withdrawal limit is the minimum of the followings:

- 24 month’s basic wages and DA for the purchase of the site. For purchase of house/flat/construction: 36 month’s basic wages and DA

- Total of employee and employer share with interest

- Total cost of the house

Also Read: Five Smart Ways How to Check EPF Balance Online Easily

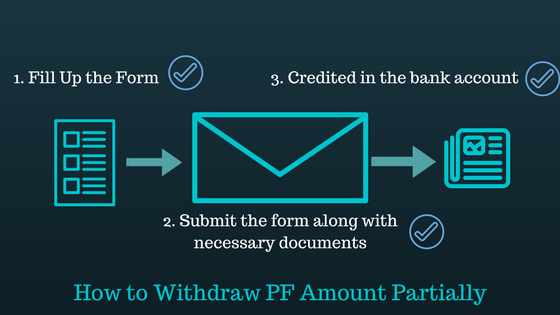

You have to fill up the form 31 and submit the same to the EPFO or employer for withdrawal.

2. Repairing/ Improvement of House:

The member can withdraw partially from PF when he or she wants to repair or alter the residence. It can be availed two times as per the followings:

- Five years from completion of house

- Ten years from availing the above

The house should be in the name of member or spouse or jointly with spouse. You have to fill up the form 31 to claim the benefit and the amount applicable is the minimum of the followings:

- 12 month’s basic wages and DA

- Employee Share with interest

- Cost of repairing/ alterations of house

3. Repayment of Existing Home Loan:

You can use the PF amount to repay your home loan. If you are too uncomfortable with your present level of EMI and want to reduce the EMI, this can help you in a big way. Though it is not wise to prepay the home loan considering the present interest rate somebody can think of it who needs a debt free life.

You need to complete ten years of service or membership to avail this benefit and you will get the chance of availing this once only.

You are eligible for the minimum of the following amount:

- 36 month’s basic wages and DA

- Total of employee and employer share with interest

- Total outstanding principal and interest of the home loan

You have to apply with form 31 and the payment will be directly done to the lender i.e. bank or NBFC where from you had taken the home loan.

Example:

Suppose, you are getting a gross salary of Rs 1 lakh per month. Out of this, your basic pay and DA is Rs 30,000 combining both. Now, in this case, 36 months basic wages and DA is RS 10,80,000. If you don’t have this much money in your account and you have only Rs 8 lakh in your EPF account, then you will get Rs 8 lakh for the repayment of the loan.

Also Read: PF Made Easy- All About EPF UAN or Universal Account Number

4. Grant of advances in special case:

You can have non-refundable advance from EPF, if the company is closed for more than 15 days, or you are not getting salary continuously for more than two months. If the company is closed for more than 6 months and you are unemployed, you can the advance. The following conditions are applicable in this case. You can avail this benefit when you face this situation. There is no restriction on how many times you are using this facility. There is no requirement on the minimum membership period also.

| Purpose of Withdrawal | Amount Eligible | Document required with Form 31 |

| In case of lockout/closure of establishment for more than 15 days, And The employees are rendered unemployed without compensation OR Employee has not received wages for more than 2 months continuously (for reasons other than strike) | Employee share with interest | Certificate from the Employer in Certificate Form A and B, as applicable. |

| Discharge/dismissal/retrenchment of member challenged by him/her in Court | Maximum 50% of Employee share with interest | Copy of petition filed in the Court and certificate from member that the case is pending |

| In case of establishment’s closure for more than 6 months and employees continue to be unemployed without compensation | Up to 100% of Employer Share with interest | Certificate from the Employer in Certificate Form A and B, as applicable |

5. Marriage of Self/ Children/ Siblings:

You can withdraw your PF for the marriage purpose. The marriage is applicable for you, children and siblings. You have to complete the seven years of service to be eligible for withdrawing this amount. But, you cannot withdraw the full amount what has been accumulated so far in the PF account.

You can withdraw only 50% of your contribution (with interest) towards PF and the withdrawal is applicable for a maximum of three times in your life. You have to fill up the form 31 and submit to EPFO for withdrawal of amount.

6. Education of Children:

You can withdraw 50% of your contribution (with interest) to meet the education expenses of your children. Post-matriculation education is applicable in this case. The minimum completed year of service is seven.

You can withdraw the amount a maximum of three times combining education of children and marriage as stated above, in your membership tenure. A certificate regarding course of study and estimated expenditure from Head of Institution is to be submitted to EPFO to avail the withdrawal.

7. Medical Hospitalization:

Medical causes are one of those for which you can withdraw your PF partially. If you don’t have health insurance and some major illness or hospitalization has happened to you or your family member, you can withdraw EPF to pay the bill.

Any of the following cases are applicable for the withdrawal

- Hospitalization for one month or more

- Major surgical operation in hospital

- Suffering from T.B., leprosy, [paralysis, cancer, mental derangement or heart ailment] and having been granted leave by his employer for the treatment of the said illness.

You can withdraw this amount at any point of time in your membership tenure. But there is a limitation on the withdrawal amount. You can withdraw the least of the followings:

- Six months’ basic wages and Dearness Allowance (DA)

- Employee contribution with interest

You have to provide the following documents to avail the benefit:

- The employer certifies that the Employees’ State Insurance Scheme facility and benefits are not available to the member or the member produces a certificate from the Employees’ State Insurance Corporation to the effect that he has ceased to be eligible for cash benefits under the Employees’ State Insurance Scheme.

- A doctor of the hospital certifies that a surgical operation or, as the case may be, hospitalisation for one month or more had or has become necessary [or a registered medical practitioner, or in the case of a mental derangement or heart ailment, a specialist certifies that the patient is suffering from T.B., leprosy, paralysis, cancer, mental derangement or heart ailment.

If the EPFO officer or the authorized subordinate to the officer is not satisfied with your provided medical certificate, he or she can ask another medical certificate to his satisfaction.

8. Physically Challenged Members:

Those who are physically handicapped can get the advance from EPFO for purchasing any equipment which will minimize the hardship faced by the candidate on account of handicap. There are no criteria for a minimum tenure of membership in this case. It can be availed for the second time after three years of availing the first benefit. The eligible amount is a minimum of the followings:

- 6 month’s basic wages and DA

- Employee Share with interest

- Cost of equipment

You have to submit a medical certificate from competent medical practitioner to avail this non- refundable advance.

9. Withdrawal within one year before Retirement:

If you have attained 54 years of age and away from retiring the service less than one year, you can withdraw PF partially.

It can be availed for once in a lifetime and you can withdraw 90% of the accumulated corpus.

Also Know: PPF Withdrawal Rules and How to Withdraw from PPF Account

Taxation of EPF Withdrawal:

If you withdraw your PF amount within five years of becoming a member, you will be liable to pay the income tax. Income tax of 10% is applicable for the person with PAN and 30% for the members without PAN. If the withdrawal amount is below Rs 30,000 there is no tax, you have to pay. You can always submit the form 15G/ 15H as applicable for not deduction of tax if your income with the withdrawal amount is below the basic exemption limit of income tax.

Withdrawal Procedure:

The member has to fill up the form 31 with the necessary document as applicable for the purpose in which you are applying. You have to fill up the form with PF account number, bank account number in which you want your money to be deposited and other details. Recently EPFO has launched a new composite form for full as well as partial withdrawal from PF. The new form is with two versions, one is AADHAAR based and another is for those who don’t have AADHAAR.

Also Read: How to withdraw PF Amount with UAN Number

Conclusion:

PF amount is for your retirement. It is always advised not to withdraw any amount of PF corpus before retirement. Moreover, with the introduction of UAN, the services related to EPF have become smooth and easy. You can easily combine the EPF accounts with single UAN. Provident fund is the greatest source of retirement and you have done your retirement fund calculation based on the PF amount. If you withdraw some of it also, it can lead to you a different situation during retirement.

Hence, when you are in a situation requiring money, think of a separate source, make a proper plan, have some contingency amount and do health insurance for hospitalization.

Share the article with others. If you have any experience or suggestion, please comment below in the comment box.

{kind=link}